You can tell a lot from a country from the tenor of its economic debate: its dominant ideologies, the leanings and structure of its media class, the power of influential players — and the quality and biases of its prominent institutions and economists.

In the case of the role of profits in inflation — currently motivating the Reserve Bank to drive the Australian economy into a wall — it also demonstrates how rank denialism can overcome seemingly prestigious bodies when it is the only way to counter fundamental threats to their core beliefs.

The RBA wants to wish the entire profit-inflation debate away, seemingly enraged at the suggestion that gouging by firms with high levels of market power is a greater spur to inflation than the traditional villain: greedy workers demanding pay rises driving a wage-price spiral.

The most the RBA will accept — as per its statement on Tuesday defending yet another rate hike — is that gouging is possibly a cause of inflation and it will keep an eye on things. But it has gone to great lengths to show that, while possible, it ain’t happening. It devoted an entire section of its most recent statement of monetary policy to discrediting the argument that profits played a significant role.

Big business has insisted that the RBA is right and their hands are clean when it comes to inflation — they’re hapless victims like everyone else of surging prices. Treasury has joined in the denialism as well.

Business cheerleaders at The Australian Financial Review — where the only good worker is a dead worker, and presumably an underpaid, immiserated, precariously employed one at that — have joined in, attacking groups like the Australia Institute, which has produced hard evidence of the role of profits.

Simply wishing away evidence because it doesn’t accord with one’s core beliefs is a hallmark of denialism, whether it relates to vaccination, the climate emergency or what’s happening in the real economy. And no one, not even central bankers or academic or bank economists, is immune to it.

But elsewhere, central banks are actively engaged in the debate about the role of profits, rather than following RBA governor Philip Lowe’s example and sticking their head under the covers. In March, the European Central Bank (ECB) released research showing:

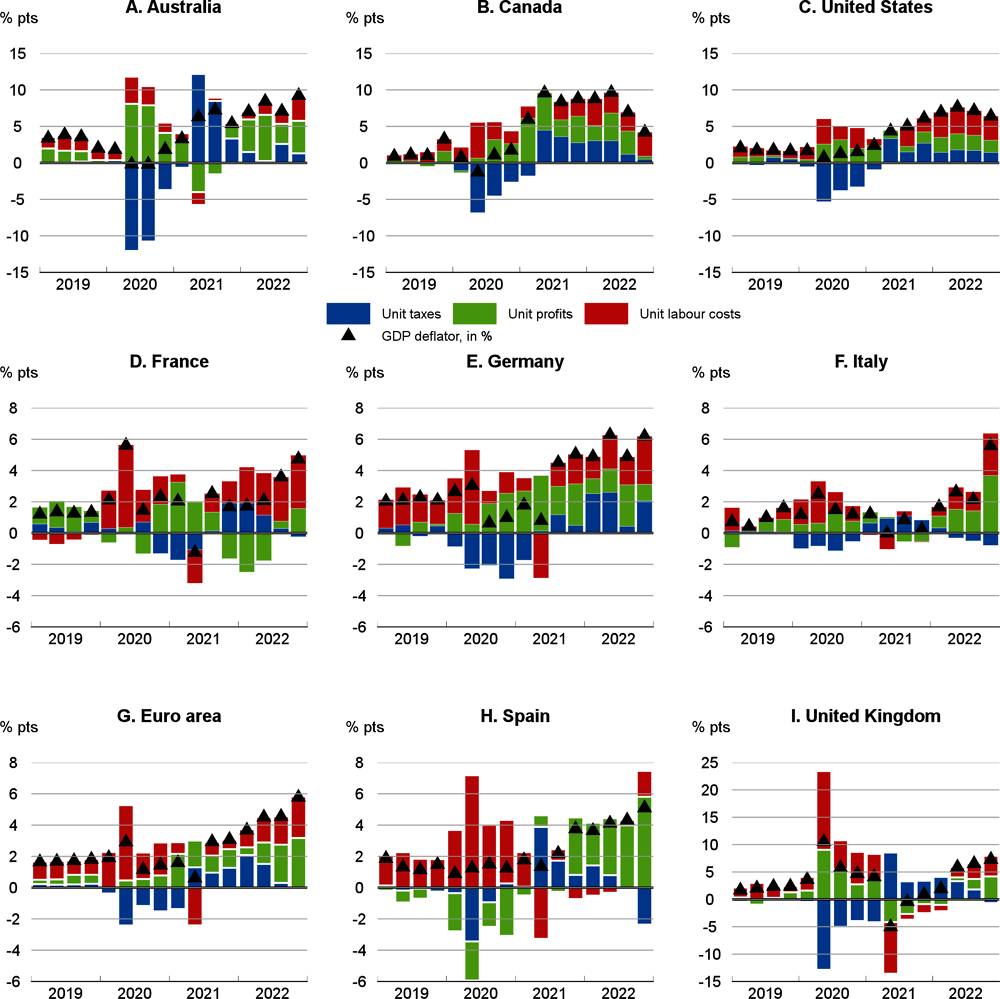

The latest increases in the GDP deflator have been driven by both unit labour costs and unit profits. Unit profits increased by 9.4% in the fourth quarter of 2022, year-on-year, and contributed more than half the domestic price pressures in that quarter, while unit labour costs increased by 4.7% and contributed less than half.

Earlier this week, ECB president Christine Lagarde went further, saying, “Sectors have taken advantage to push costs through entirely without squeezing on margins, and for some of them to push prices higher than just the cost push”.

Lagarde made the same point that many proponents of the profit-inflation link had made, that businesses had exploited “a situation of ‘everybody’s in the same position, we’re all going to raise prices’”. That is, rising prices caused by supply-side shocks like the Ukraine war have provided cover for firms with market power to raise prices beyond levels needed to maintain margins.

She also lamented the lack of data on the role of profits in inflation versus wages — effectively admitting that central bankers were more worried about the latter than the former. Not much denialism there.

It’s not just the Europeans: the Kansas Fed produced a paper in January showing that “markup growth was a major contributor to inflation in 2021. Specifically, markups grew by 3.4% over the year, whereas inflation, as measured by the price index for personal consumption expenditures, was 5.8%, suggesting that markups could account for more than half of 2021 inflation.”

The Kansas Fed did argue that it was less a case of business exploiting market power than preemptively raising prices in anticipation of future rises. And more recently it suggested the effect had declined in 2022 — though it was still a noticeable impact.

And overnight, the OECD weighed into the debate, devoting a section of its latest global economic forecasts to the issue. Its data specifically on Australia shows unit profits massively outweighing unit labour costs as a source of inflation. Oops — how embarrassing.

The core argument of the RBA et al in wishing the problem away is that you have to ignore mining and energy profits because everyone knows that’s a special case — mining profits have inflated the overall profit share of income versus the wage share of income, and energy prices have generated enormous profits, but only due to Putin and the Ukraine war.

But regardless of the merit of removing the biggest demonstration of exactly the point your opponents are making — that a highly concentrated industry is exploiting market power to generate massive profits, in this case, an industry that’s a critical input into the costs of businesses right across the economy — the problem is that the RBA is left inside the Pythons’ “What have the Romans ever done for us?” scene.

If we omit energy, what about other structurally important inputs to the economy? Late last year, the Australian Competition and Consumer Commission found that stevedores’ profits had soared higher prices, and suggested market concentration had enabled them to exploit pandemic disruptions. Yesterday, construction materials giant Boral celebrated its capacity to lift prices as a key reason for surging profits.

What about for consumers directly? How about grocery prices: Coles and Woolworths have enjoyed surging profits off increasing prices higher than inflation. The banks have also enjoyed higher profits off the higher cost of money imposed by the RBA — something Lowe thinks is a good thing. Then there’s Qantas, which posted a massive profit on the back of, by the admission of former CEO Alan Joyce, higher airfares. And department stores — struggling a few years ago — now enjoy strong profits off higher prices.

In the spirit of John Cleese, that leaves Lowe, after he’s finished raging at today’s OECD report, demanding: “Apart from energy, freight, construction materials, groceries, interest rates, airfares and retail, where’s this so-called profit-driven inflation?”

And remember this bout of profit-driven inflation comes at the end of a near-decade of wage suppression, and a historic shift — especially since 2017 — from wages to profit share of income nationally. Merely preserving, let alone strengthening, profit margins in a period of high inflation perpetuates that shift from workers to business.

As Lagarde hints, all this sits poorly with central bankers’ received wisdom of how contemporary markets work, and their relative indifference to the power that large corporations in concentrated markets have (something the RBA itself recently pointed out). Neoliberals have a blind spot when it comes to market concentration: the core idea that unfettered markets work more efficiently than highly regulated markets means a relative antipathy to effective competition laws designed to protect the very mechanism by which markets work efficiently.

In the RBA and Lowe’s case, the blind spot has turned into rank denialism — when their counterparts elsewhere are taking the issue very seriously indeed.

And as the Reserve Bank keeps jacking up interest rates in pursuit of inflation driven by powerful corporations rather than the greedy workers of central banker stereotype, the cost of that denialism for Australians keeps going up. Lost jobs. Mortgage defaults. Divorces. Yet more inequality. And, inevitably, despair and suicides of people who face a bleak financial future.

Like vaccine denialism, or climate denialism, the RBA’s denialism has a cost that will be counted in lives.

Does the RBA have it right or is its head in the sand? Let us know by writing to letters@crikey.com.au. Please include your full name to be considered for publication. We reserve the right to edit for length and clarity.

{kind=link}

Welcome back Bernard

Yes! Welcome back, Bernard. We have missed your columns and this is one of your best.

An essential read, welcome back Bernard.

Has it ever occurred to readers, that in effect, we are living in a capsule once defined as The Lunatic Asylum? We have Lowe in denial, telling the poor to spend less and get an extra job, we have the Aukus nightmare, we have the SMH/Age-led warmongers urging us to make war on China and we have the US nominally led by a man who finds it difficult to put three words together, Biden, and we have what any sane human can only describe as a US Proxy war on Russia. Where, I wonder, will it all end? Oh, and Climate Change – let’s build another Coal Mine, Tanya…

Thankfully human beings tend to progress despite the idiots who lead them.

Well said Bernard. Even Ross Gittins said the same this week in the SMH. People like P. Lowe and that irritating talking head Innes Willox just love to lay the boot into the wage earners blaming them for this inflation run. But you won’t hear boooo out of them when it comes to talking about record corporate profits contributing to inflation. By intentionally omitting corporate profits from their inflation narrative, they are complicit in lying to the Australian people to protect their mates in big business.

Well said. It is intolerably frustrating that Willox is given a platform to espouse his blatantly misleading opinions without being l questioned or challenged with any serious intent. Every time he speaks it’s just an infomercial.

My blood is boiling. How’s yours?