As the Reserve Bank of Australia (RBA) has been left further and further behind by international institutions in its denialism about the role of corporate profits in inflation, there’s been a growing question of not merely how long it would remain in denialist mode, but how exactly it would try to catch up to the US Federal Reserve, the European Central Bank, the OECD and others.

The minutes from its June meeting suggest it was starting that process even as the OECD was humiliating it by detailing the huge role profits had played in Australian inflation, compared with wages.

It was just a start, though. The denialism remains deep at Martin Place.

The minutes devote considerable space to wages growth and the possibility it could feed inflation. Even workers simply getting wage rises that match inflation would be “concerning”, the minutes said — not merely do we need to see hundreds of thousands of Australians lose their jobs, workers need to suffer yet more real wage cuts. The minutes devote 300 words specifically to worrying about wages, a word that occurs over a dozen times. How often does “profit” occur? Not at all. But the minutes do, near the end, contain this gem:

Members discussed the possibility of implicit indexation of wages to past high inflation and the potential for this to become widespread. Similarly, members observed that some firms were indexing their prices, either implicitly or directly, to past inflation. These developments created an increased risk that high inflation would be persistent, which would make it more difficult to keep the economy on the narrow path.

So the RBA admits that firms are pushing prices up higher than inflation, causing persistent high inflation. Of course, it doesn’t say this is about maintaining profits, the implication is mere carelessness on the part of firms — oops, we’ve increased prices by 2021 levels! Damn! That this leads to higher profits is, presumably, a mere byproduct of that carelessness. Insert shot of a shocked, shocked, Claude Rains being handed his winnings in Casablanca.

But the fact that firms are doing this to the extent that even big business’ mates on the RBA board noticed it only comes after the possibility that wages growth might push inflation up is discussed yet again. For the RBA, the mere possibility that wages growth might push inflation up is worth hundreds of words of analysis, but the reality that profits are driving inflation up gets a couple dozen words — and both are equated as equal risks to inflation.

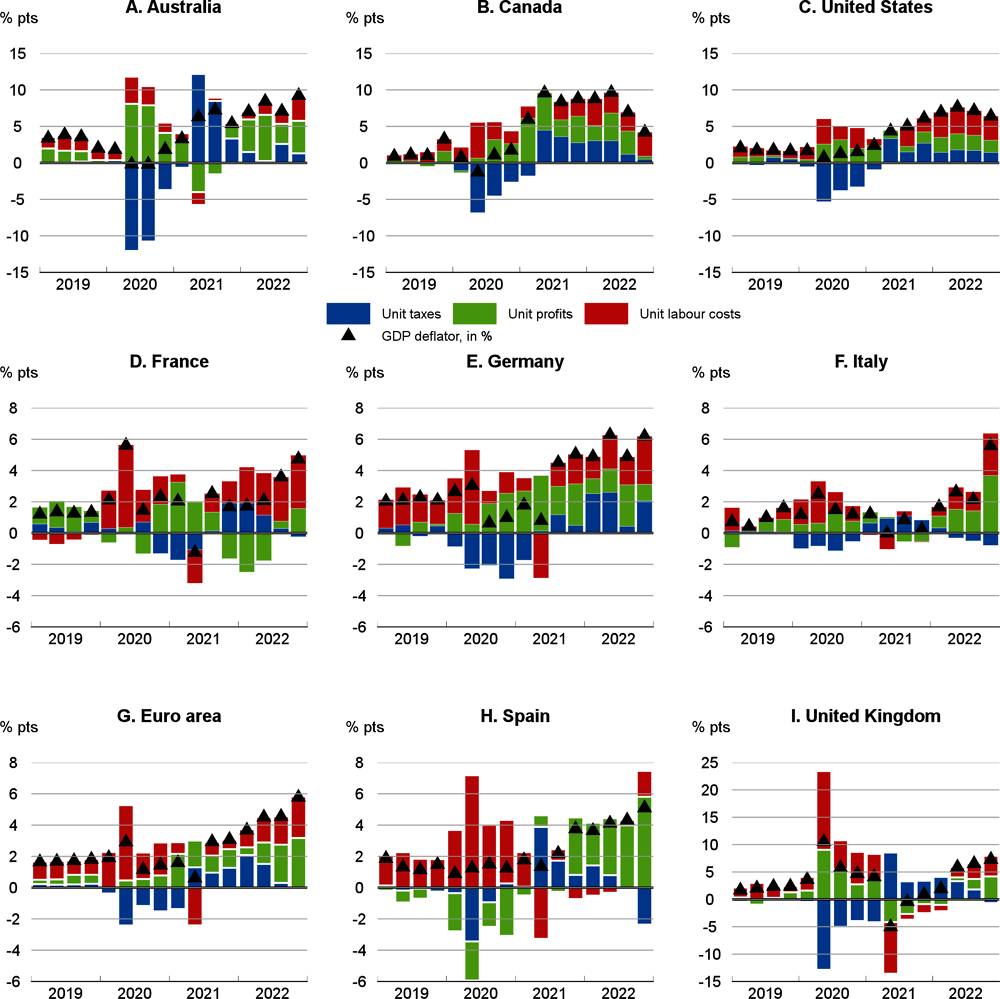

As we know from the OECD’s data, profits have played more than twice the role that wages have played in driving up Australian inflation over the past few quarters. They’re not even close to equal in terms of impact.

It’s nice of the RBA to end its blanket denialism and catch up with the rest of the world in recognising price gouging by firms is causing inflation — sorry! increasing the risk of inflation. But it’s still locked into its neoliberal worldview that the real problem is always those horrible workers wanting pay rises.

For an institution that is supposedly obsessed with inflation, you’d think it would pay a lot more attention to what’s causing it, rather than rereading 1970s economics textbooks.

{kind=link}

yeah! I was visibly shocked this morning.

I read that Child Care facilities were putting up their prices, to coincide with the Government increasing the Child Care allowance.

What a coincidence.

And we know that the bulk of income from child care centres goes to the execs running them, not to workers, although worker pay rises will be the justification they use to keep their profit margins.

and these scum werehanded non competitive access to private development sites through the directors or same their relatives who are the developers of the childcare centres which append units and shopping centre which give the profiteers the special investment dollars to do these destructive business coopting land, rights, childcare should be community and free

yes and who privatisedchildcare beyond the neo libs in both major parties- but yes Kennett trally cleaned out public assets but labor too – vote Greens or cross progressives to out 2 party govt cartels

The RBA have been lead kicking and screaming to the realisation that it is price gouging and profit taking that is causing most of the inflation we are seeing in the economy. They are still gas lighting workers, warning of a potential for a wages-prices spiral, now they are wnting the unemployment rate to rise from 3.7% to 4.5%, putting an extra 100,000 full time workers at least out of work. In their latest incarnation to vary their themes of punching down, they are now lying some lip service to the role of business in inflation. Particularly those business sectors which have enormous market power and coverage. I won’t hold my breath on them holding press conferences and knifing their own Board members in the back, some of whom were appointed by the coalition and some of whom are members of free-market, right wing think tanks and lobbyists like the Minerals Council of Australia or the IPA. This I would have to see. Let’s see how far their criticisms of business extend.

Our market is beholden to our two major retailers who control a major part of our supply chain and purchases. They set the prices and we must follow.

Same could be said with the major airline, banking, petrol retailers. We are being royally screwed with out any lubricant. I apologies for the vulgar analogy but it is just the way I feel, Every one clips the ticket, and we pay.

its the epitome of violence against women , then men – the onesstuck in the middle and at the fringes

slimy flim flam merchants

Of course the CEO’s of those price gouging profiteering companies don’t notice inflation because they were happy to give themselves a 15% pay rise.

Aha, this executive bonus-inflation spiral is getting out of hand, we need a Fairer Work Commission to reign this in … before the price of a Ferrari gets beyond the reach of your average government consultant.

Thank you BK. Keep spreading the work about this.

I will second this. Keane, you were sorely missed.

I think we are way past the point where they have successfully suppressed the inflationary pressures exerted by the not-well-off’s increased expenditure on luxury items like eating out, a modest holiday, or a new telly, if they were there to start with.

Now they are working on suppressing those other luxury items like food, shelter and energy.

They’re like doctors who decide the only way to save the patient is to cut off oxygen, food and water, and get that pesky heartbeat to go away.

It’s the only way to save the patient!

What kind of a crazy economic system do we have, which requires people to starve, to save it? What kind of system is it, that vilifies the jobless when unemployment is at 5%, but then actively tries to get the number of unemployed back up there because “too many people have jobs”?

It’s clear, that their idea of economic utopia in perfect balance, is: low inflation + stagnant wages + 5% unemployed (without adequate welfare)…with the happy side-effect that the cohort of already very wealthy are given free rein to hoover up all the newly created wealth as it comes out of this perfect economic engine. I mean, you can’t have that wealth going anywhere else, can you? it causes INFLATION, and then where would we be? The billionaires are doing us a social service really!

It makes you wonder how there could ever have been a 30 year period after WW2 where this wasn’t a problem… it’s like the immutable laws of reality had a little break for 3 decades, before being restored.

Now, we have the perfect ever-lasting circulatory system, that must be maintained at all costs, and never tampered with…and, of course, fingers crossed that pesky climate change stuff doesn’t wreck it all and force any unpleasant changes!

I read today where business is booming for RIviera, a Gold Coast luxury yacht builder – sales have increased more than 500% over the past decade. Price of their yachts ranges from $1.1m to $6.9m. No dampening of demand there.

Maybe the workers are with a multimillionaire job provider on one of the 6 new plum contracts- provided uni educated disabled workers – paying em zero per week as work for the dole ! good for em it is assumed because it is “a job”- Eric Abetz said so – but what is a university educated man being abused as unemployable and then told he will be labelled as disabled to keep it on the down low ; like ” older workers” if you are 45? or 62? You are an older worker and thats why you dont derserve a living paypacket